| 일 | 월 | 화 | 수 | 목 | 금 | 토 |

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | ||

| 6 | 7 | 8 | 9 | 10 | 11 | 12 |

| 13 | 14 | 15 | 16 | 17 | 18 | 19 |

| 20 | 21 | 22 | 23 | 24 | 25 | 26 |

| 27 | 28 | 29 | 30 |

- 이것이 코딩테스트다

- pandas

- sklearn

- scikit learn

- 태블로

- 데이터 분석

- 자격증

- 이코테

- 시각화

- Google ML Bootcamp

- 파이썬

- 코딩테스트

- 통계

- ML

- ADsP

- Python

- r

- pytorch

- matplotlib

- 딥러닝

- tableau

- IRIS

- 데이터 전처리

- 머신러닝

- SQL

- Deep Learning Specialization

- 데이터분석

- 데이터분석준전문가

- 회귀분석

- SQLD

- Today

- Total

함께하는 데이터 분석

[EDA] FA with R 본문

안녕하세요!

오늘은 Factor Analysis의 약자인 FA에 대해 알아보겠습니다.

파일은 저번이랑 똑같은

이 파일입니다. 만약 파일 정보가 필요하시다면

2022.02.06 - [분류 전체보기] - [EDA] PCA with R

[EDA] PCA with R

오늘은 Principal Component Analysis 일명 PCA에 대해 간단한 예제를 R을 통해 알아보는 시간을 갖겠습니다! 그러기에 앞서 필요한 파일을 첨부하겠습니다. 위 데이터는 주식에 관한 10개 회사의 값입니

tnqkrdmssjan.tistory.com

여기서 확인해주세요!

그럼 시작하겠습니다.

### perfrom factor analysis with 3 factors but without any rotation

kval<-3 #앞서 PCA와 hclust의 결과를 토대로 3개의 factor로 해보기

stock.FA<-factanal(scale(stocks), kval, rotation="none")

## varimax rotation (orthogonal rotation)

stock.FAr1<-factanal(scale(stocks), kval, rotation="varimax")

## promax rotation (oblique rotation)

stock.FAr2<-factanal(scale(stocks), kval, rotation="promax")여기서는 앞서 PCA와 hclust의 결과를 토대로 3개의 factor로 분석했지만

만약 결과를 알 수 없을 땐 2, 3, 4, 등등 여러 가지 경우를 돌려보고

유의미한 factor 개수를 찾아야 합니다.

FA를 할 때 rotation 종류에 따라 3가지 방법 no rotation, varimax, promax이 있습니다.

그중 가장 유의미하다고 생각되는 것을 골라서 사용하면 됩니다.

## with no rotation

with(stock.FA, plot(loadings[,1], loadings[,2], xlim=c(-1, 1), ylim=c(-1,1),

main="Stocks (No rotation)", xlab="Factor 1", ylab="Factor 2"))

with(stock.FA, text(loadings[,1], loadings[,2],labels=1:10, pos=4))

abline(v=0); abline(h=0)

with(stock.FA, plot(loadings[,1], loadings[,3], xlim=c(-1, 1), ylim=c(-1,1),

main="Stocks (No rotation)", xlab="Factor 1", ylab="Factor 3"))

with(stock.FA, text(loadings[,1], loadings[,3],labels=1:10, pos=4))

abline(v=0); abline(h=0)

위의 경우는 rotation을 하지 않은 경우인데 그래프를 보면

구별하기 쉽지 않은 것을 알 수 있습니다.

stock.FA$loadings

>>> Loadings:

Factor1 Factor2 Factor3

comp1 0.889 0.237 -0.235

comp2 0.713 0.386

comp3 0.335 0.278

comp4 0.309 0.111 -0.191

comp5 0.628 -0.664 0.148

comp6 0.473 -0.638

comp7 0.113 -0.542

comp8 0.640 0.167 0.496

comp9 0.236 0.529 0.577

comp10 0.110 0.168 0.552

Factor1 Factor2 Factor3

SS loadings 2.613 1.773 0.999

Proportion Var 0.261 0.177 0.100

Cumulative Var 0.261 0.439 0.539

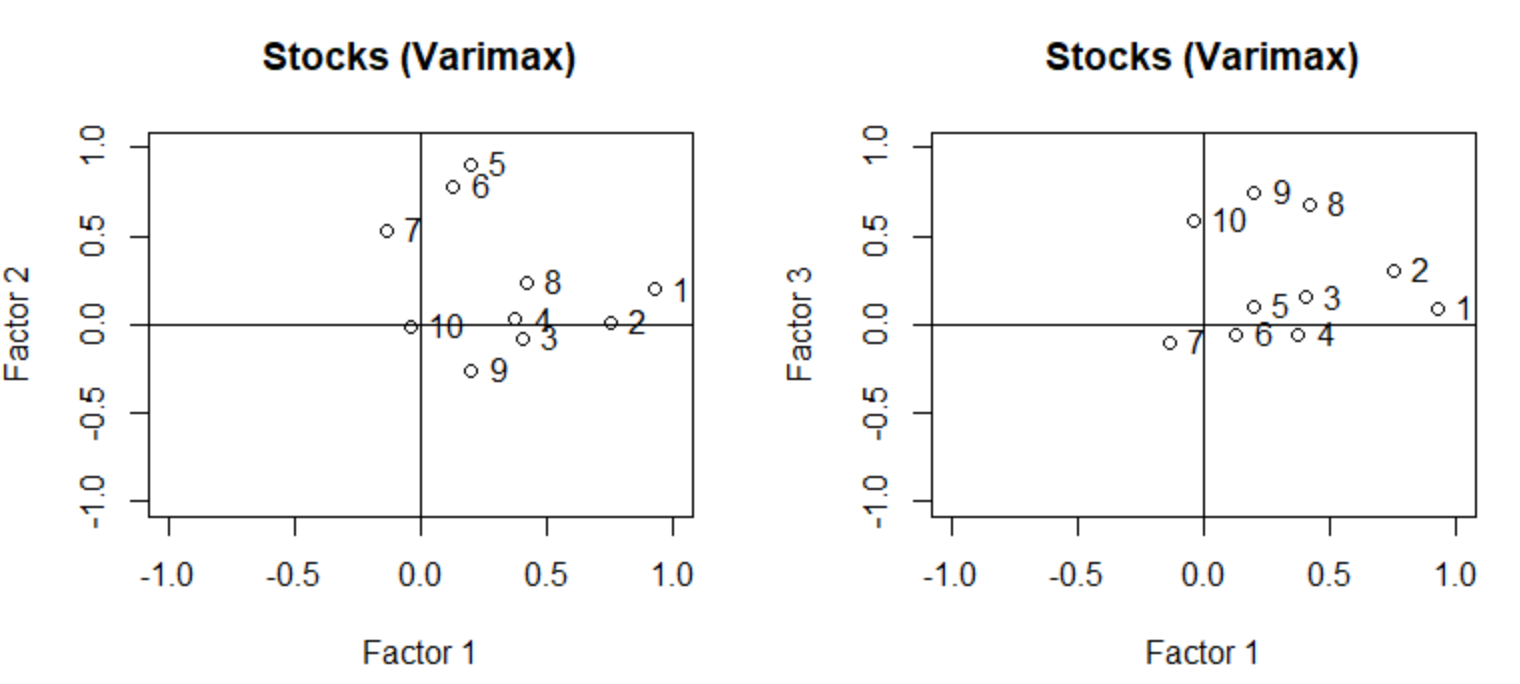

## with varimax

with(stock.FAr1, plot(loadings[,1], loadings[,2], xlim=c(-1, 1), ylim=c(-1,1),

main="Stocks (Varimax)", xlab="Factor 1", ylab="Factor 2"))

with(stock.FAr1, text(loadings[,1], loadings[,2],labels=1:10, pos=4))

abline(v=0); abline(h=0)

with(stock.FAr1, plot(loadings[,1], loadings[,3], xlim=c(-1, 1), ylim=c(-1,1),

main="Stocks (Varimax)", xlab="Factor 1", ylab="Factor 3"))

with(stock.FAr1, text(loadings[,1], loadings[,3],labels=1:10, pos=4))

abline(v=0); abline(h=0)

위의 경우는 varimax rotation을 사용한 경우인데 첫 번째 그래프를 보면

comp5, 6, 7이 뭉쳐있고 Factor2가 큰 것을 확인할 수 있습니다.

stock.FAr1$loadings

>>> Loadings:

Factor1 Factor2 Factor3

comp1 0.924 0.197

comp2 0.751 0.305

comp3 0.401 0.151

comp4 0.374

comp5 0.195 0.899 0.103

comp6 0.126 0.782

comp7 -0.140 0.526 -0.102

comp8 0.418 0.238 0.673

comp9 0.200 -0.260 0.749

comp10 0.586

Factor1 Factor2 Factor3

SS loadings 2.009 1.869 1.508

Proportion Var 0.201 0.187 0.151

Cumulative Var 0.201 0.388 0.539comp1, 2, 3, 4는 Factor1

comp5, 6, 7은 Factor2

comp8, 9, 10은 Factor3의 값이 큰 것을 확인할 수 있습니다!

즉, 각각의 Factor가 해당하는 회사에 유의미하게 작용한다는 것을 알 수 있죠.

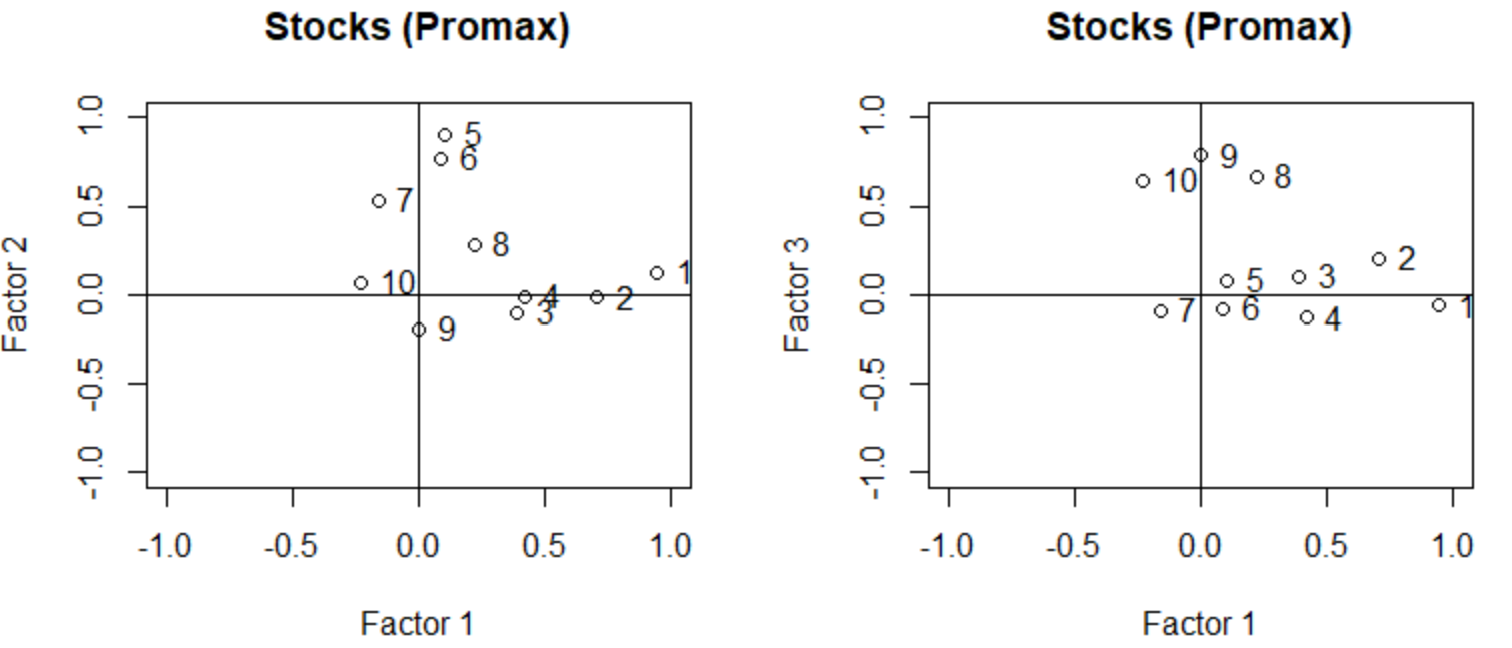

## with promax

with(stock.FAr2, plot(loadings[,1], loadings[,2], xlim=c(-1, 1), ylim=c(-1,1),

main="Stocks (Promax)", xlab="Factor 1", ylab="Factor 2"))

with(stock.FAr2, text(loadings[,1], loadings[,2],labels=1:10, pos=4))

abline(v=0); abline(h=0)

with(stock.FAr2, plot(loadings[,1], loadings[,3], xlim=c(-1, 1), ylim=c(-1,1),

main="Stocks (Promax)", xlab="Factor 1", ylab="Factor 3"))

with(stock.FAr2, text(loadings[,1], loadings[,3],labels=1:10, pos=4))

abline(v=0); abline(h=0)

마지막으로 promax rotation입니다.

첫 번째 그래프에서 comp5, 6, 7이 Factor2에 영향을 받고

두 번째 그래프에서 comp8, 9, 10이 Factor3에 영향을 받는다는 것을

쉽게 볼 수 있죠!

stock.FAr2$loadings

>>> Loadings:

Factor1 Factor2 Factor3

comp1 0.945 0.121

comp2 0.706 0.206

comp3 0.388

comp4 0.416 -0.130

comp5 0.102 0.902

comp6 0.771

comp7 -0.162 0.532

comp8 0.217 0.284 0.664

comp9 -0.188 0.785

comp10 -0.229 0.648

Factor1 Factor2 Factor3

SS loadings 1.860 1.836 1.569

Proportion Var 0.186 0.184 0.157

Cumulative Var 0.186 0.370 0.527이 결과를 보더라도 위의 no rotation, varimax rotation보다 더 쉽게

결과를 도출할 수 있죠.

이처럼 3가지 rotation 중 본인이 분석할 때 더 유의미하다고 생각되는 것을

사용하면 됩니다.

감사합니다!

'통계학과 수업 기록 > EDA' 카테고리의 다른 글

| [EDA] PCA with R (0) | 2022.02.06 |

|---|---|

| [EDA] SVD with R (0) | 2022.02.05 |

| [EDA] K-Means Clustering with R (0) | 2022.02.02 |

| [EDA] Hierarchical Clustering with R (0) | 2022.02.02 |